Some claim that British American Tobacco (BAT) is one of the best passive income stocks around.

Each year since 1998, the cigarette giant has increased its payout to shareholders. This means it belongs to an exclusive club of Dividend Aristocrats, stocks that have achieved at least 25 years of dividend growth.

And during its four most recent financial years, it’s managed to boost its annual payout by an average of 3.3%.

Should you invest £1,000 in Halma Plc right now?

When investing expert Mark Rogers has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for nearly a decade has provided thousands of paying members with top stock recommendations from the UK and US markets. And right now, Mark thinks there are 6 standout stocks that investors should consider buying. Want to see if Halma Plc made the list?

However, despite this impressive performance, it might come as a surprise to learn that there’s another FTSE 100 stock that’s done even better.

Who’s that then?

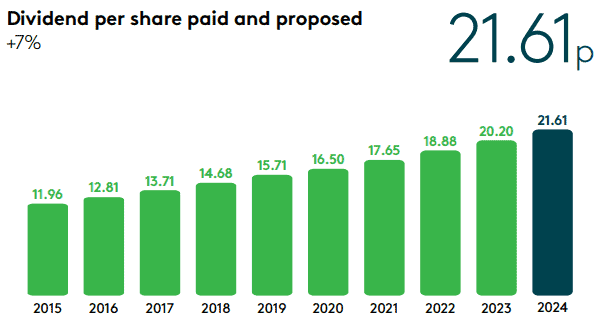

Halma (LSE:HLMA), the life-saving technology company, has increased its dividend by at least 5% a year for an incredible 45 years.

But despite this amazing track record, I don’t consider it to be an income stock.

That’s because it’s currently (8 October) yielding only 0.9% — way below the FTSE 100 average of 3.8% and, for example, that of British American Tobacco (8.7%).

However, I’m not going to immediately dismiss the idea of investing.

Halma’s yield is low because its share price has grown significantly in recent years. Since October 2014, it’s more than quadrupled, which makes it sound like a growth stock to me.

And with its share price currently 22% below its all-time high achieved in December 2021, now could be a good time to consider taking a stake.

How does it grow?

Halma buys small and medium-sized businesses with a global reach, in its niche markets of safety, health and the environment.

Since 1971, it’s bought over 170 companies and claims to have another 600 in its pipeline. Through acquisitions alone, the group has a target of adding at least 5% to earnings each year.

Its most recent purchase was Rovers, a Dutch business that designs and manufactures specialist devices that help detect cervical cancer at an early stage.

For the year ended 31 March 2024 (FY24), Rovers generated a profit after tax of £3.8m on sales of £10m. Assuming all targets are met, Halma will pay £77m for the company. This is a multiple of 20.2 times earnings.

This sounds expensive for a private company but it should see an uplift in the group’s stock market valuation, even if nothing changes. That’s because for FY24, Halma reported earnings per share of 82.4p, meaning the group currently trades on a historic price-to-earnings ratio of 30.3.

Therefore, all things being equal, the acquisition of Rovers will add £115m (30.3 x £3.8m) to Halma’s market cap. With a price tag of ‘only’ £77m, shareholders could soon start to benefit.

Caution

However, as with any investment, there are risks.

We’ve seen that the shares aren’t cheap and its yield is low.

Also, its return on capital employed was 1.9 percentage points lower in FY24, than in FY14. This means it’s having to work harder just to stand still.

My verdict

But over the past 10 years it’s grown both revenue and earnings by an average of 11% a year.

And I believe the markets in which it operates — particularly healthcare and the environment — could be some of the strongest over the next decade or so.

For these reasons, I’m going to put the company on my watchlist for when I’m next in a position to invest.